●●●●

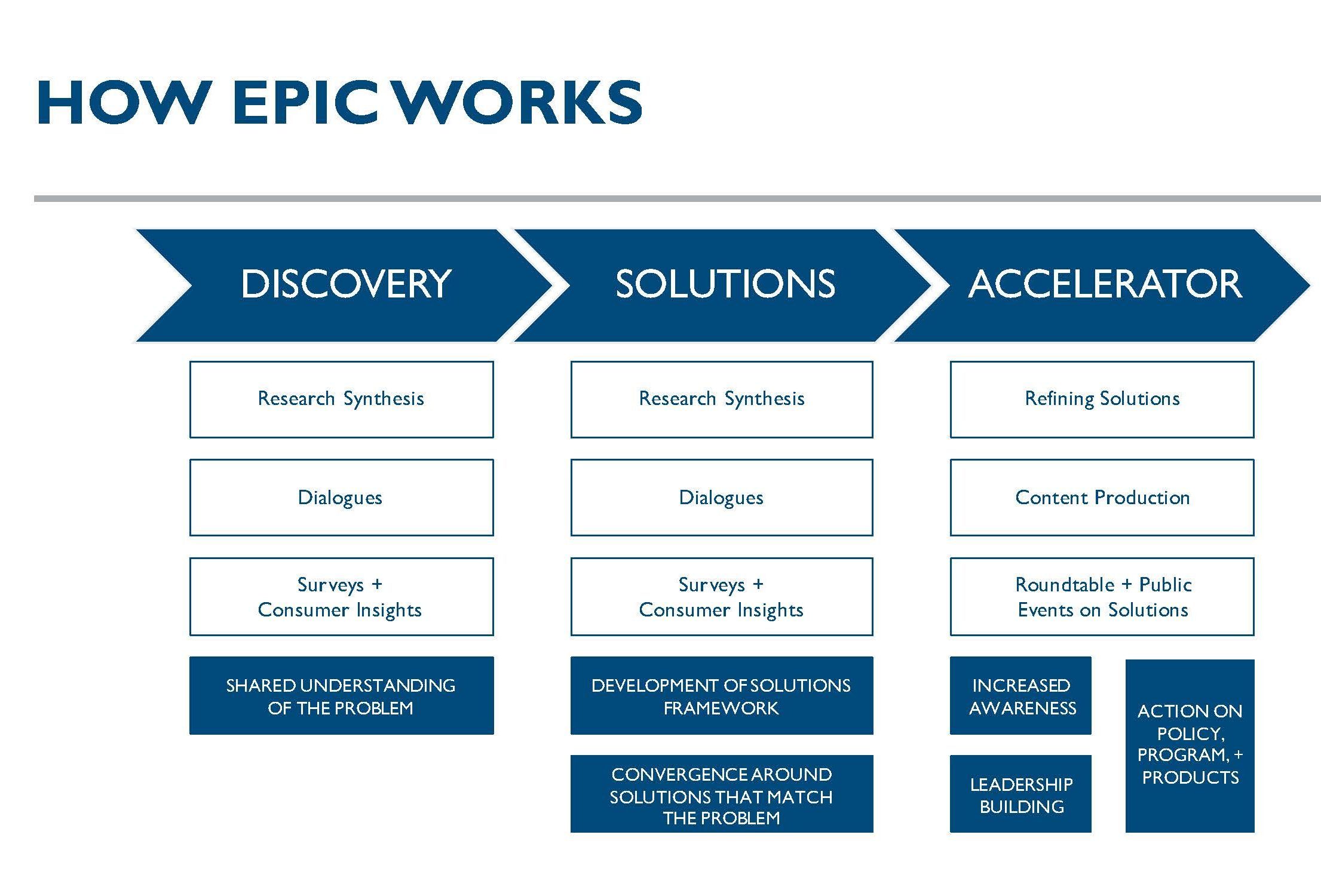

PHASE ONE | LEARNING & DISCOVERY

● Primer

Executive Summary

The Aspen Institute’s Expanding Prosperity Impact Collaborative (EPIC)—an interdisciplinary approach to illuminating and addressing critical aspects of household financial insecurity—is focusing on consumer debt. EPIC is studying this issue now because consumer debt has reached record highs amid an economy more robust than at any point since the end of the Great Recession. Unemployment is at historic lows and wages are up, leading to many rosy interpretations of current debt trends. Yet signs continue to point to the fragility of many families’ finances, and households’ experiences with debt in the current economy vary widely on demographic and geographic lines. This is a critical moment to better understand the changing dynamics of consumer debt, how households are managing the debt they are carrying, and the conditions under which it is a source of financial insecurity versus an opportunity for future mobility.

EPIC’s particular focus is on non-mortgage consumer debt, such as loans to pay for college or to purchase a vehicle, money borrowed on credit cards, and non-loan debt (i.e. municipal fines and fees, medical debt, and unpaid bills). Non-mortgage debt has not received the extensive attention given to housing borrowing, largely because the size of the mortgage market. However, housing debt is declining as a share of household debt and current causes for concern—such as rising rate of serious delinquency in credit cards and the emergence of subprime auto loans—relate to other areas of the market. This primer distills the research on consumer debt, from its drivers and its dimensions to its impacts on households and society as a whole. EPIC will use this critical knowledge base to articulate a framework for developing solutions to improve the financial lives of millions of Americans.

● Convening

Key Findings

Roughly 30 experts from the private, public, and nonprofit sectors came together to discuss the state of consumer debt research, the biggest drivers and impacts of consumer debt, whether certain types or amounts of consumer debt pose a danger to household financial health, and the possible influence of macro economic trends on consumer debt. Watch our video series below.

● Research

● Events

PHASE TWO | SOLUTIONS

● Solutions Framework

Executive Summary

Consumer debt is ubiquitous. Although at any given time some Americans are debt-free, most of us carry debt some or even all of the time. We borrow for various reasons, and we are increasingly likely to incur debt also from non-loan sources (such as an out-of-pocket medical expense or being assessed a governmental fine or fee. Consumer debt is not inherently bad (taking on debt can often be a sound financial decision), but it is a concern today because it has reached record levels, and its effects reach deeply into financial security, physical and mental health, as well as the broader economy. Consumer debt is a systemic problem with significant consequences, but there are systemic solutions. With solutions ranging from product-level improvements to broader reforms, EPIC has identified options for stakeholders in every sector and for partnerships across sectors. Collectively, these solutions possess tremendous potential to address a critical dimension of household financial insecurity.

This inability to meet basic needs with income from labor, transfers, and other sources makes it difficult to maintain emergency savings and appears to push many households into debt. Moreover, these same households often rely on more expensive and higher-risk forms of debt, such as payday loans, subprime auto loans, and private student loans.

Our work on consumer debt includes a focus on the drivers, features, and consequences of household debt among these financially vulnerable households.

● Research

● Events

PHASE THREE | ACCELERATION

● Research and Events

● Our Funders

EPIC’s work is supported by the Annie E. Casey Foundation, the MetLife Foundation, Prudential Financial, the W.K. Kellogg Foundation, and by the Aspen Institute Financial Security Program’s other core funders.

● Our Team

Learn more about the team behind EPIC by visiting AspenFSP.org and scrolling down to see the full Aspen FSP team.

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved